Cash’s retreat and contactless’s rise are reshaping in-person commerce: cash fell from 44% of in-store spend in 2014 to 15% in 2024, while digital wallets reached 30% of point-of-sale spend in 2023, according to Worldpay’s Global Payments Report 2024. For Tier-2/3 Banks and Digital Transformation Seekers, three intertwined trends—SoftPOS, Tap‑to‑Phone, and network tokenization—will define global mobile payments in 2025–2027.

This outlook focuses on the global market and is tailored to regional small and mid-size banks seeking practical roadmaps to modernize acceptance, reduce fraud, and lift authorization rates—without compromising compliance or customer trust.

-

-

Why These Trends Matter Now

As mobile technologies increasingly power the real economy—contributing 5.8% of global GDP per GSMA—the acceptance layer is undergoing a structural upgrade. Standards are mature, device capabilities are ubiquitous, and card networks report measurable benefits from tokenization. The net result: faster deployments, lower total cost of ownership, and improved payment outcomes for merchants and banks.

Deep Dive: Core Trends (2025–2027)

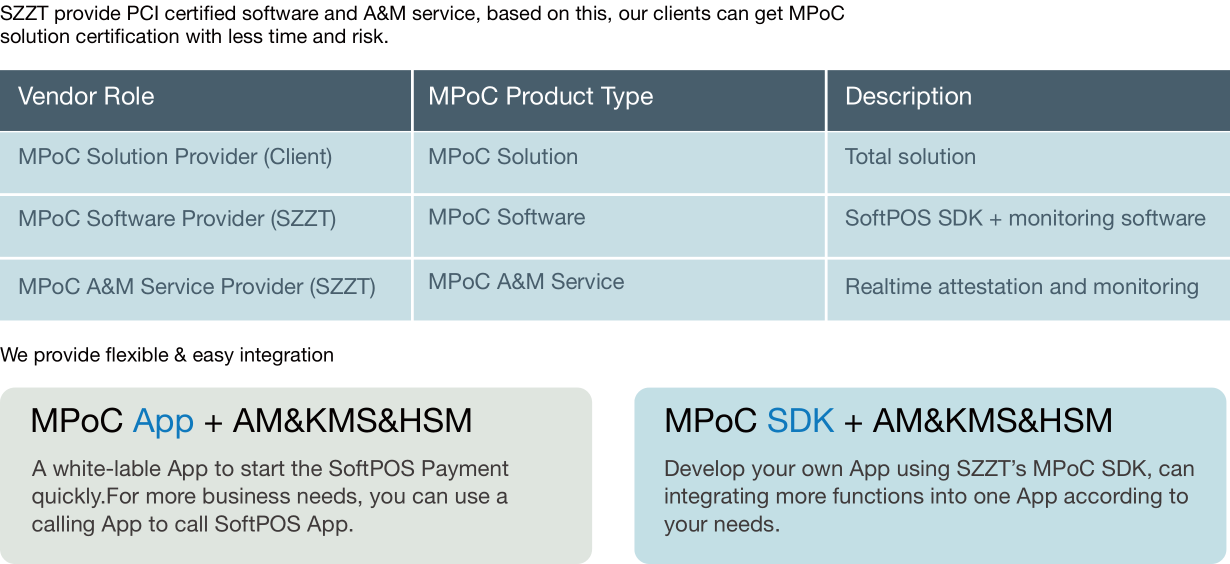

SoftPOS: Software-Defined Acceptance on COTS Devices

SoftPOS enables merchants to accept contactless card payments on commercial off-the-shelf (COTS) devices (smartphones/tablets) with no dedicated hardware. The PCI Mobile Payments on COTS (MPoC) standard provides an objective-based security framework for solutions supporting contactless and PIN on the same device, building on earlier SPoC and CPoC standards.

Drivers include NFC ubiquity, lower capex versus dedicated terminals, rapid onboarding for micro and small merchants, and mature compliance testing through PCI-recognized labs. For banks, SoftPOS accelerates merchant acquisition, especially in underserved segments.

Data points: PCI SSC formally published MPoC and continues to update the program (e.g., v1.1), improving integration, testing, and management requirements (PCI SSC).

Value chain impact: device OEMs and ISVs align on SDKs; acquirers streamline provisioning; merchants reduce hardware costs; consumers gain consistent tap experiences.

Tap‑to‑Phone: Contactless Everywhere

Tap‑to‑Phone brings contactless acceptance to any compliant smartphone, enabling mobility, queue-busting, and embedded commerce use cases. Adoption momentum is strong: Visa reported 200% year‑over‑year growth worldwide in 2025, with additional innovations such as Tap‑to‑Add‑Card catalyzing token enablement.

Drivers include consumer familiarity with contactless (billions of annual contactless transactions in markets like the UK), merchant mobility needs, and lower barriers to entry. For Tier‑2/3 Banks, Tap‑to‑Phone is a “tech equalizer” for SMB portfolios.

Value chain impact: acquirers expand acceptance rapidly; PSPs bundle Tap‑to‑Phone into omnichannel propositions; merchants unlock flexible checkout; consumers experience consistent tap flows.

Network Tokenization: Security with Better Payment Outcomes

Tokenization replaces sensitive PANs with network tokens, reducing exposure and enabling lifecycle management. The EMV® Payment Tokenisation Technical Framework defines roles, flows, and the Payment Account Reference (PAR) to link tokenized transactions to the underlying account.

Measurable benefits are now documented at scale. Visa reports tokenized card‑not‑present transactions see a ~30% reduction in online fraud and a ~4.6% lift in authorization rates versus PAN credentials (Visa). Token issuance is accelerating, enabling more frictionless updates and fewer failed payments (Visa Acceptance).

Value chain impact: issuers improve approval and fraud outcomes; acquirers gain more stable credentials; merchants reduce false declines; consumers enjoy seamless renewals.

Data‑Driven Outlook (Global, 2025–2027)

-

-

Evidence points to continued global expansion of contactless acceptance and tokenized credentials. Regulatory pressure and fraud trends (see McKinsey’s Global Payments Report) will push banks to invest in authentication, data sharing, and standards‑aligned acceptance.

| Item | Evidence | Source |

|---|---|---|

| Digital wallets at POS (2023) | 30% share | Worldpay GPR 2024 |

| Cash in-store share | 2014: 44% → 2024: 15% | Worldpay |

| Tokenization outcomes | ~30% online fraud reduction; ~4.6% authorization lift | Visa |

| Tap‑to‑Phone momentum | 200% YoY global growth (2025) | Visa |

| SoftPOS standard maturity | PCI MPoC v1.1 program available | PCI SSC |

Opportunities and Challenges

Opportunities

- SMB acquisition at scale via SoftPOS and Tap‑to‑Phone, lowering onboarding friction.

- Improved payment outcomes from network tokens (higher approvals, lower fraud).

- Embedded commerce and mobility for field sales, delivery, and events.

- Portfolio differentiation for Tier‑2/3 Banks through standards‑aligned solutions.

Challenges

- Compliance complexity across PCI MPoC, EMV, and device security baselines.

- Fraud management requiring data, biometrics, and consortium participation (McKinsey).

- Change management for merchant support, training, and service operations.

- Legacy integration and token lifecycle orchestration with existing platforms.

Practical Action Guide

For strategic decision‑makers (CEOs/CFOs of regional banks)

- Prioritize SoftPOS/Tap‑to‑Phone acceptance to expand SMB reach with lower capex.

- Mandate network tokenization across card‑not‑present flows to lift approvals and reduce fraud.

- Invest in analytics and data partnerships to strengthen authentication and reduce false declines.

For managers (Payments, Risk, IT)

- Select MPoC‑listed solutions and verify lab certifications for SoftPOS deployments (PCI SSC).

- Enable token lifecycle management (updates, credential refresh) and PAR alignment per EMVCo.

- Benchmark authorization and fraud KPIs using network token data (e.g., VisaNet insights).

For general audiences

- Adopt contactless habits; choose merchants supporting Tap‑to‑Phone and tokenized checkouts.

- Keep devices updated and use trusted wallets to benefit from secure tokenized credentials.

Value Realization with SZZT ELECTRONICS CO., ЛТД.

SZZT ELECTRONICS CO., ЛТД. is a financial technology solutions provider (est. 1993) with core strengths in payment terminals, self‑service kiosks, platform services, mobile payment and SoftPOS solutions, and intelligent banking/hospital solutions. The brand serves clients across five continents, 160+ countries, with 10M+ devices shipped and 300+ patent applications, backed by certifications including CMMI, ISP, VISA, PCI, and CE.

For Tier‑2/3 Banks and Digital Transformation Seekers, this means a partner capable of standards‑aligned SoftPOS/Tap‑to‑Phone rollouts, tokenization‑ready platform integration, and robust after‑sales operations that protect portfolio economics while elevating customer experience. To tailor these trends to your market, request an expert consultation or start an inquiry.

References

- Standards bodies: PCI Security Standards Council (MPoC); EMVCo Payment Tokenisation.

- Networks: Visa Tap‑to‑Phone growth (2025); Visa tokenization outcomes; Visa Acceptance.

- Market analysis: Worldpay Global Payments Report 2024; Worldpay 10‑year trends; McKinsey Global Payments Report.

- Decision support: Gartner (Hype Cycles, Magic Quadrants, diagnostics, and expert guidance for faster, smarter technology decisions).